I sometimes see news articles and opinion pieces about where gold might go in the next week, or month, or even year. But if you’ve ever spoken to one of our dedicated Account Executives here at U.S. Money Reserve, you know that owning gold doesn’t have to include worrying about the next week, or month, or year. Historically, gold ownership functions well as a long-term strategy—and if you’re anything like me, you believe that long-term strategies matter most when it comes to wealth, retirement, and protecting the futures of those you love.

While there are certainly times when gold prices have shot up quickly—especially during times of market and economic disruption, like in 2011 and 2020—gold’s real power lies in its ability to diversify your portfolio and realize growth potential over years or even lifetimes.

As we continue to celebrate U.S. Money Reserve’s 20th anniversary, let’s look back at the last 20 years of gold to see why gold may serve you best in the long run.

Gold has grown significantly over the last 20 years—and not just in response to movements in the stock market.

As I write this, gold is currently back up over $1,800/oz. Last year, in August 2020, gold hit its all-time high of over $2,072/oz. As Australia’s Perth Mint put it back in January 2021, “Whilst [gold’s annual growth in 2020 was] a very solid return, it is not unexpected.” Perth Mint was considering gold’s history of growth within similar economic environments—specifically, environments in which low interest rates have fueled fears of increased inflation. If that sounds familiar, it should—we’re in a similar economic environment right now.

In last week’s Gold News & Views, I wrote about the current state of our national debt—how it has increased over the last 20 years and how gold has performed in that same amount of time. If you didn’t catch it, here’s the piece of information I want to repeat: Since January 2001, gold has increased more than 570%. That’s a huge increase, and any individual with gold in their portfolio was surely happy to see gold’s price increases, especially in 2011 and 2020 when gold reached all-time highs. Regardless of how much gold you have in your portfolio, those types of increases can mean a world of difference for your financial future.

But there’s something we didn’t talk about last week that I’d like to point out. Take a look at this chart:

Source: Macrotrends

While you can see those peaks, you’ll also notice that from 2000 to 2011, gold was on a steady (and impressive) upward slope. The same thing happened from around 2015 to the all-time high in 2020. Clearly, gold does more than just react to inflation or short-term gains or losses on the stock market. It’s also an impressive asset in its own right—and one many use as a diversifier in their portfolio.

Gold can become an important part of your retirement portfolio.

As you may have heard me say before, I pay extremely close attention to the wellness of our team and ensure that I’m doing everything I can to support and challenge them. But there’s another part of my job—the part that involves numbers and logistics. So when I read the August 31, 2021, article by CNBC that said, “The Social Security trust fund most Americans rely on for their retirement will run out of money in 12 years, one year sooner than expected, according to an annual government report,” my mind immediately went into planning mode. What would this mean for myself and my children? What would it mean for our employees and customers? It’s never too early to consider these sorts of topics.

What I came away with was this: Diversification matters more than ever. With debt and the rate of inflation increasing, we all need to ensure that our wealth is protected. And while everyone’s financial situation—and thus their asset mix—is unique, we must all do everything we can to make sure we and our loved ones are as prepared as possible for whatever is waiting for us in the years to come.

This is why, once again, I encourage you to look to gold’s history as a store of wealth and a source of positive growth potential. All assets have their ups and downs, and I would never encourage anyone to bet their entire future on a single asset, but by diversifying with gold and other precious metals, you allocate a portion of your wealth to a time-tested safe-haven asset that may not react to market fluctuations in the same way as stocks or bonds.

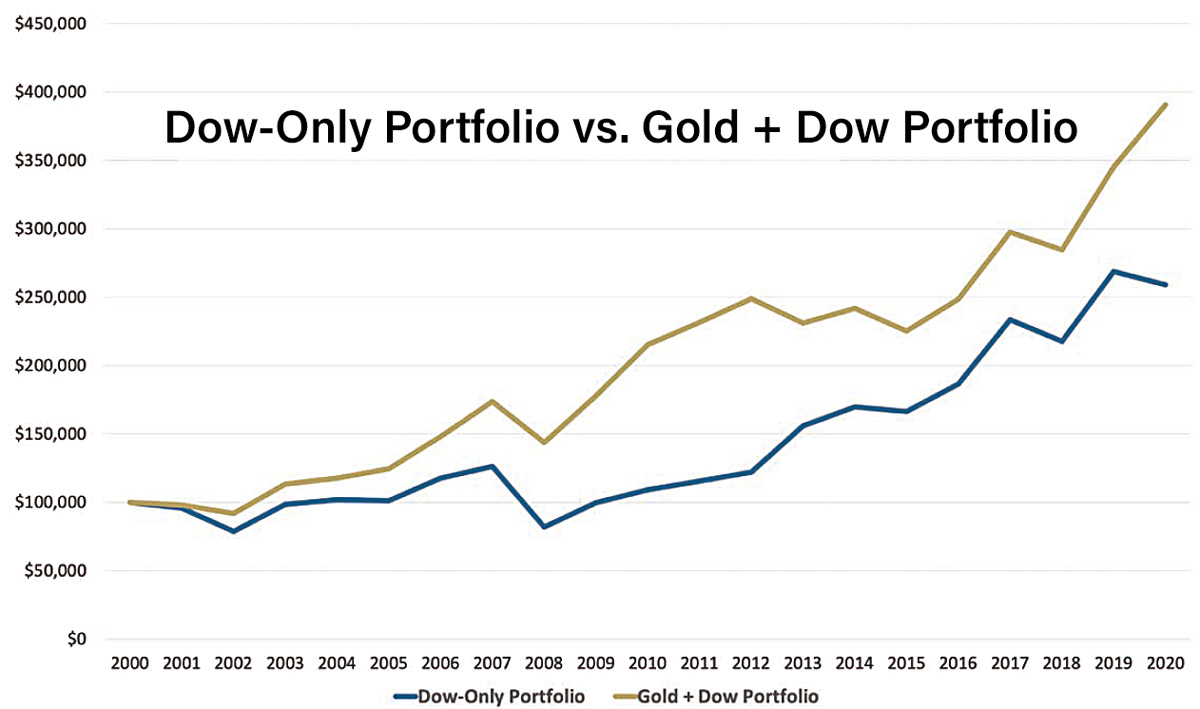

Source: Date range from 10/27/00 to 08/07/20. Kitco, Yahoo! Finance, Reuters. Based on an allocation of 75/25 stocks (Dow)/gold.

There’s a reason Reuters wrote on July 15, 2021, that “central banks now hold more than 35,000 metric tons of [gold], about a fifth of all the gold ever mined”—and a reason this news is worthy of our attention. As history has shown us, gold can play an incredibly important role in portfolio diversification. And when the world’s banks begin to make moves toward gold, it means someone in their organization—someone whose entire job is to study the economy and make suggestions—believes that gold is the right choice, right now.

And while everyone’s portfolios and acceptable levels of risk are different, many of us have the same goals: to retire comfortably and leave something behind to help future generations.

Gold is a time-tested form of generational wealth.

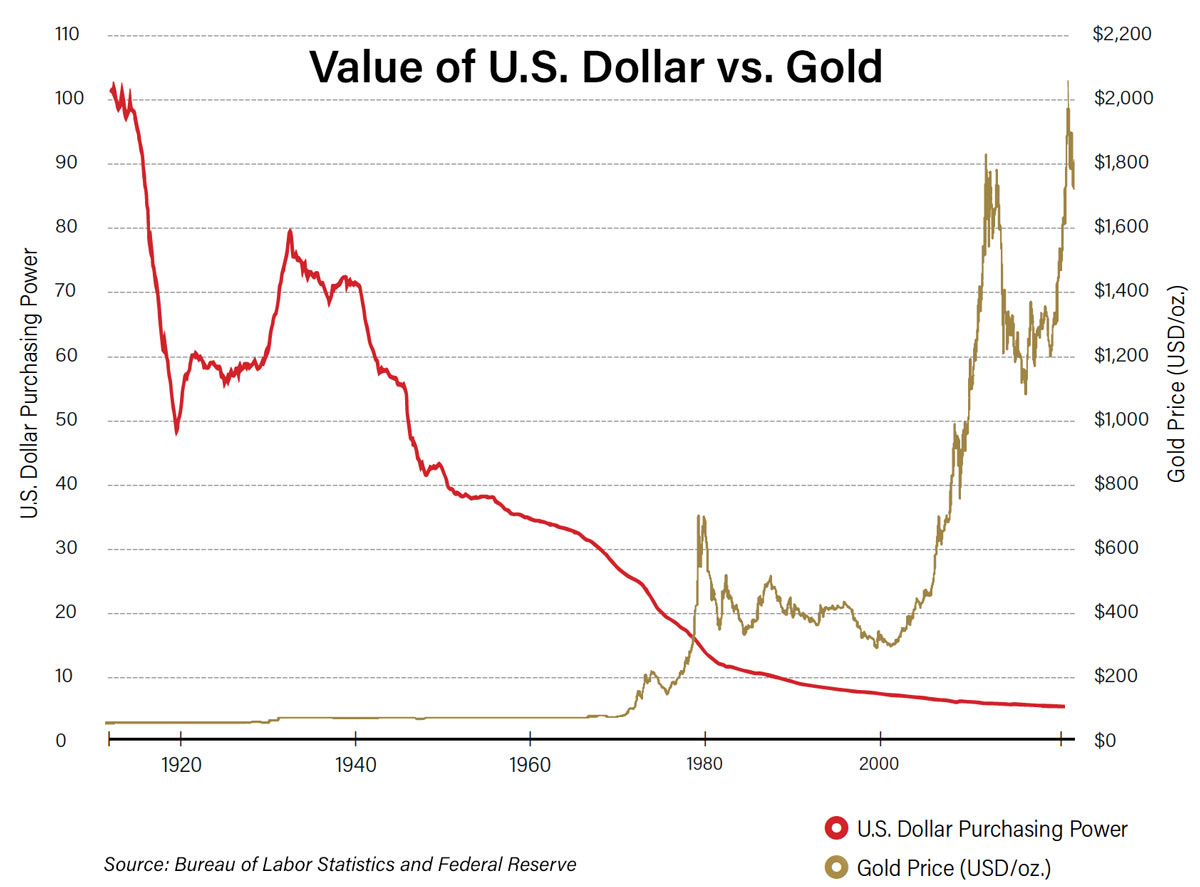

Historically, gold grows over the long term, holding onto its purchasing power, while the U.S. dollar weakens. So when the time comes to pass your wealth on to future generations, would you rather have all of your eggs in one basket or hold a diversified portfolio that lowers your overall risk?

Again, I’m not suggesting that your legacy take only the form of gold. But if prices continue to rise, your cash will continue to buy less and less with every year—and if the rate of inflation beats the rate of interest on your cash holdings, you’ll effectively be losing money over the long term. But over the last 20 years, gold has grown by leaps and bounds, from around $270/oz. to more than $1,800/oz. Who’s to say where gold might go in another 20, 40, or 60 years?

One cannot deny the power that gold and other precious metals hold over the long term, especially in the face of growing economic concerns like inflation and national debt.